November 14, 2018

I want to save for my retirement; what type of plan should I use? A traditional IRA or a Roth IRA—or another vehicle?

Saving for retirement is a big subject and important for every person to think about, plan for, and execute. If this topic is not currently relevant to you, it likely is to one of your family members, whether a spouse, sibling, a child, or even a grandchild. While Social Security benefits can serve as an important part of income during retirement, for many retirees these funds are not sufficient to cover expenses during retirement years. Historically, many workers could count on pensions, programs in which companies would “save” on behalf of employees during working years and then “return” these funds to employees during retirement years. These “defined benefit” plans have largely been replaced by “defined contribution” plans such as 401(k)s and Individual Retirement Accounts (IRAs), which place most of the responsibility for retirement savings and planning with the employee.

“One of the key questions for many is whether to use a traditional IRA or a Roth IRA.”

This fundamental shift of responsibility from companies to employees makes it important for workers to have a basic understanding of the retirement vehicles that are available to them as individuals accumulate savings while working and plan to access those funds during retirement. The primary options are IRAs, Roth IRAs, 401(k)s, Roth 401(k)s, and 403(b)s. One of the key questions for many is whether to use a traditional IRA or a Roth IRA. As we explore this question in some detail, keep these two points in mind:

- A key factor in the choice between a traditional IRA and a Roth IRA is whether one’s tax rate will be lower during working years or in retirement.

- Having options can be beneficial, so consider having both a Roth IRA and a traditional IRA.

“...any funds contributed to one of these accounts grow tax-deferred or tax-free while in the account.”

Some of the principles of traditional IRAs and Roth IRAs are the same. In both cases, any funds contributed to one of these accounts grow tax-deferred or tax-free while in the account. This means that no taxes are paid on the capital gains, dividends, or interest that is earned inside the account. In the case of traditional IRAs, income taxes are deferred until withdrawals of funds begin, while withdrawals from Roth IRAs are not taxed because the funds were already taxed when they were put into the account.

A key differentiator between the two is the required minimum distributions (RMDs) that must be taken from a traditional IRA beginning at the age of 70 ½. In the first year, about 3.6% of the account value (IRA value divided by 27.4, according to Internal Revenue Service tables) is distributed and recognized as taxable income. This contrasts with Roth IRAs, for which there are no required distributions. Under current law, distributions are 100% tax-free because taxes were paid on the original earnings.

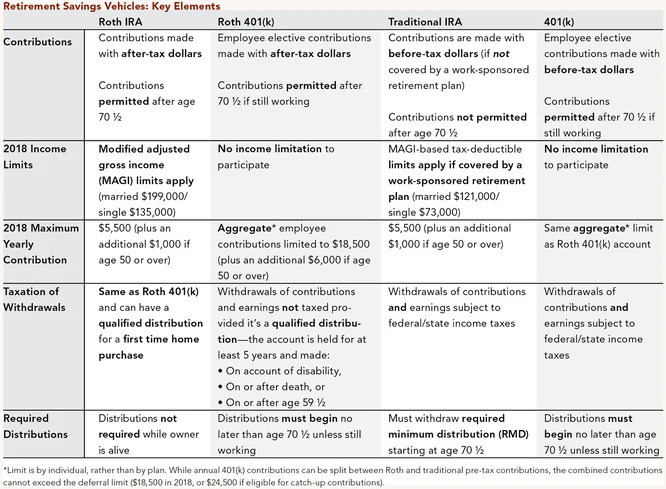

BASIC FEATURES OF RETIREMENT SAVINGS VEHICLES

Named after Delaware Senator William Roth (thank you Bill!), Roth IRAs were established with the Taxpayer Relief Act of 1997. A Roth IRA is a type of retirement plan in which after-tax dollars are contributed to an account. These funds grow tax-free until used, and upon use are not taxed at the federal or state level. Funds can be left in a Roth IRA for the owner’s entire life and be passed to the next generation. The maximum amount that can be contributed to a Roth IRA is the lesser of the owner’s earned income for the year or the limits noted in the table on the following page. There are also income limits for Roth IRAs. For those above the income restriction levels, a Roth 401(k) might be utilized if offered by one’s employer.

Traditional IRAs were established as part of the Employee Retirement Income Security Act of 1974 (ERISA). The before-tax contribution limits for traditional IRAs are identical to those of Roth IRAs, and, like a Roth IRA, the owner (or the owner’s spouse) must have earned income of at least the same amount as the contribution. A key point is that if neither member of the couple is covered by a retirement plan at work, the traditional IRA contribution is deductible. However, if either is covered by a work-sponsored plan, then modified adjusted gross income (MAGI) based limitations apply to the deduction. However, “after-tax” contributions can still be made.

The other retirement vehicle for which the Roth concept applies is a company sponsored 401(k) plan. A 401(k) plan is a defined contribution plan in which an employee can contribute either before-tax or after-tax dollars. Similar to IRAs, no taxes are paid on capital gains, dividends, or interest while the investments are in the plan. One of the large advantages of 401(k) plans in comparison to traditional IRAs is that the contribution limits are higher and there is no income limit for the deduction. Some company plans include a Roth 401(k) option. The choice of whether to use a 401(k) or Roth 401(k) is similar to the IRA choice; it depends on one’s current versus future tax rates and desire for flexibility (the Roth offers more flexibility in the future because distributions are not required). Basic elements of these retirement savings vehicles are summarized in the table below.

ROTH VS. TRADITIONAL DECISION FRAMEWORK

One reason we suggest utilizing both a traditional and Roth account is because it provides the owner (the investor) flexibility. By having both traditional and Roth IRAs, an investor’s overall portfolio can be structured with stocks in the Roth account and bonds in the traditional piece. This could be done so that the higher growth assets are in the IRA that is not taxed (the Roth) and the lower growth assets are in the traditional IRA.

A traditional IRA may be worth more to a person who earns, for example, $120,000 per year than an individual with $30,000 in income per year because the higher earner receives a larger tax deduction. If the high earner takes the tax deduction savings and also invests those funds, then the longer-term value of the traditional IRA may exceed that of a Roth IRA. Again, this depends on the tax rates at contribution and withdrawal. If tax rates at withdrawal are lower, then the traditional IRA will prove more valuable.

SPECIAL CONSIDERATIONS: CHARITABLE CONTRIBUTIONS AND ROTH CONVERSIONS

For a traditional IRA, under the Tax Cuts and Jobs Act of 2017 (TCJA) the strategy of donating to charities directly from an IRA after age 70 ½ is now included in the law. The qualified charitable distribution (QCD) allows those who meet the minimum age of 70 ½ to give money to charities directly from IRAs in a tax advantageous manner. The advantages are that the QCD counts toward satisfying the RMD and the distribution is excluded from the taxpayer’s income. With fewer individuals expected to itemize deductions under the TCJA, the income tax deduction may be lost for many people. Besides the age requirement, one restriction is that the QCD is limited to $100,000 per year.

“The qualified charitable distribution (QCD) allows those who meet the minimum age of 70 ½ to give money to charities directly from IRAs in a tax advantageous manner.”

Another way to establish a Roth is to complete a conversion process from a traditional IRA to a Roth IRA. This may be more attractive today due to the lower tax rates that were a result of the TCJA. While prior to 2010 this was only allowed for those with a MAGI under $100,000, today anyone can utilize this option. A conversion involves withdrawing funds from the traditional IRA (or a portion of it) and contributing the funds to a Roth IRA. Taxes are due on the amount withdrawn for the conversion, but the funds then grow tax-free in the Roth. This process is a bit tricky, because the extra taxable amount from the traditional IRA may push a taxpayer into a higher tax bracket in the year of the conversion. Multi-year conversions are also an option that can reduce or spread out the tax implications of the change. We recommend seeking advice and assistance from one’s accountant and investment counselor before taking this step.

OTHER FAMILY-FRIENDLY WEALTH PLANNING TIPS

- Help a child or grandchild who is working set up a Roth IRA, even if he or she simply has a summer job that only pays a few thousand dollars. Following the contribution limits outlined in the table on the previous page, make a personal gift to the child or grandchild to fund the Roth IRA. This could provide multiple benefits: 1) directly enhance the younger generation member’s financial future; 2) improve the child or grandchild’s financial literacy by allowing them to learn about investments; and 3) the benefit of long-term compounding can be significant.

- Subject to joint income limits, a working spouse can contribute funds to a non-working spouse’s IRA. Therefore, if one spouse is not covered by a plan at work, the other spouse does not work, and each is over the age of 50, both the working and nonworking spouse can contribute $6,500 to an IRA and receive a deduction of $13,000 (provided the working spouse’s income is over $13,000).

- If one’s employer offers a Roth 401(k) option, consider a combination of normal and Roth 401(k) contributions.

- Roth IRAs, which are inheritable, could help build multi-generational wealth because the saver is never required to take a withdrawal, and because withdrawals are tax-free. Distributions will be required once the beneficiary inherits the IRA funds, but those distributions would be based on the heir’s life expectancy. For example, distributions for a 50-year-old heir will likely stretch out over 30 or so years. Again, for Roth IRAs all those distributions are tax-free!

CIRCLING BACK TO WHERE WE STARTED

While the exact circumstances are limitless, the key variables in the decision process for investing in a traditional IRA or a Roth IRA are age, current and retirement-based income levels and tax rates, the retirement plan offered by the employer, cash flow circumstances, and spending habits now and during retirement.

Consider Roth IRAs as a tool that may fit into a long-range financial planning picture with the potential for being a very valuable (and flexible) asset. One of the main reasons we encourage considering a mixture of Roth and traditional accounts is that with so many variables—including the possibility of changes in tax laws—having a blend can provide more options in the future.

Download Article: Many Paths, One Destination: Forging Your Way to Retirement

The above information is for educational purposes and should not be considered a recommendation or investment advice. Investing in securities can result in loss of capital. Past performance is no guarantee of future performance.