As of early-August, US stocks, as measured by the S&P 500, are up about 12% in 2024. A first-half rally wasn’t supposed to happen for a number of reasons. Entering the year, the market traded at over 19x forward earnings – not particularly cheap. The Fed Funds rate had exceeded 5% since Summer 2023, putting the growth of large pieces of the economy at risk. Inflation was still running above the Fed’s target level, leaving little reason for rate cuts. Real yields on the 10-year US Treasury were approaching 2%, their highest level since the mid-2000s, so for the first time since the Global Financial Crisis (GFC), bonds offered an attractive rate of return. The TINA (“There Is No Alternative”) phenomenon, whereby investors favored stocks due to lack of alternatives offering reasonable return prospects, was no longer in effect. To the surprise of many, stocks rose anyway. Gains occurred in line with an improving forward earnings outlook, which is healthy.

There’s one caveat: earnings growth expectations have been driven by the technology sector. Firms investing in AI capabilities or selling the proverbial AI “picks and shovels” are expected to reap massive economic benefits. Per our July 2024 Market Commentary, we believe it’s a little early to assign many trillions in market value to a few presumed winners. The short-lived technology sector sell-off on August 5th showed that other investors may be skeptical as well.

“We’ve seen signs that the US consumer, which drives about 70% of the economy, is stretched.”

The rest of the market appears to be softening. Companies outside the technology sector, on

average, are expected to show tepid earnings growth in 2024. We’ve seen signs that the US consumer, which drives about 70% of the economy, is stretched. Savings rates are down, pandemic cash cushions have been depleted, and credit card debt has jumped to over $1.1 trillion. Bellwether industrials have reported flagging demand in the first half of the year. Further to these signs of macroeconomic slowing, a tame inflation report in July increased the odds of a September rate cut. We view that as a possibility. But it does appear that the “lower for longer” rate environment that persisted from the period between the GFC and the pandemic is behind us, whether or not the economy weakens from here.

Given the aforementioned backdrop – technology sector leadership, an economy slowing at the margin, and a higher baseline for interest rates than what we’ve seen over the past 15 years, we will make two long-term predictions. The first is that a “lower for longer” interest rate environment will continue to be unnecessary to drive demand for stocks. The second is that it will pay to pick stocks outside the current crop of “big tech” names leading the S&P 500.

Regarding the first prediction, although TINA might have been a driver of money flows into equities from the GFC until mid-pandemic, “lower for longer” hasn’t been required to generate incremental buying in stocks since then. We think demographics might be a factor.

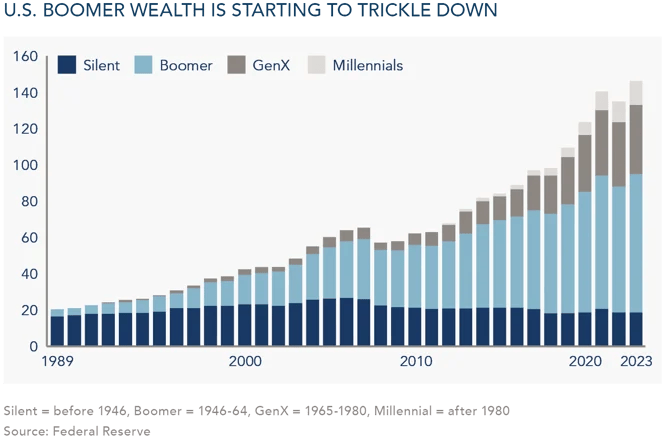

Consider the plight of the Millennial generation, born between 1981 and 1996. Many either began their careers during the dot-com bust of the early 2000s or during the GFC, or watched their parents suffer serious portfolio drawdowns during those periods. Psychological wounds take time to heal. Meanwhile, skyrocketing housing and education costs meant not much money was left over to invest.

“Millennials are enjoying the first truly strong labor market of their careers, all while wealth is starting to trickle down from older generations.”

Behind the Millennials, Generation Z, born between 1997 and 2012, doesn’t share the same scars. From crypto currencies to “meme stocks,” volatility doesn’t scare them. Speculative investments aside, the relative safety of equity ownership in cash-producing businesses will be there when they are ready. We believe that time will arrive in the years to come.

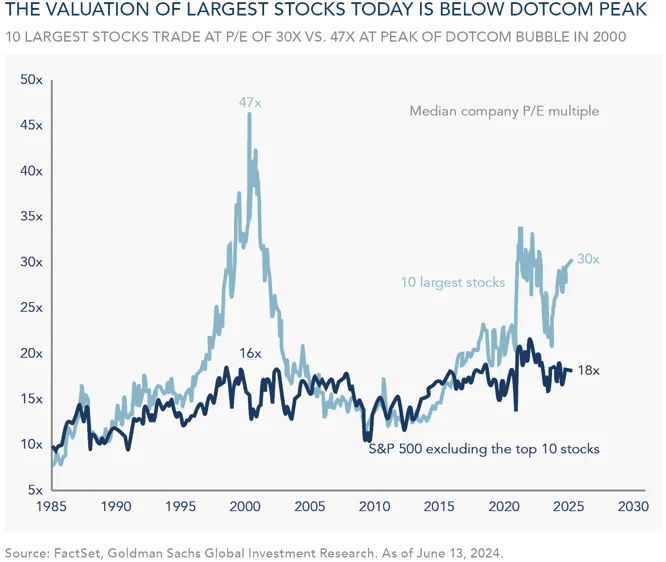

Our second prediction is that canny stock-picking outside “big tech” will pay off. For every dollar invested in an S&P 500 index fund today, about 35% gets invested in the top ten largest companies in the index, most of which are technology-driven. Further, a significant portion of the expected earnings growth from that group of ten is coming from AI-related prospects. That’s one reason why the group is valued so richly versus the rest of the index [Chart 2]. As future investment returns are highly correlated with starting valuations, we think putting a third of one’s equity allocation into expensive technology companies today is risky. AI looks likely to boost productivity and benefit vendors of such technology over the long run. But let’s not forget that a myriad of use cases aren’t yet a reality. As we noted in our July Market Commentary, McDonald’s hit pause on its AI-driven drive-thru technology due to implementation snags. And let’s remember that spending on technology capacity is cyclical. At some point, data centers will slow purchases of GPUs and re-evaluate future investment roadmaps.

To be clear, we are invested in some fine tech-forward companies that are AI beneficiaries. However, we are finding strong prospects in other areas of the market as well. Regardless of which generation our clients represent, our sights remain on protecting and growing long-term purchasing power no matter where any one sector, the broader economy, or interest rates may be headed.

The above information is for educational purposes and should not be considered a recommendation or investment advice. Investing in securities can result in loss of capital. Past performance is no guarantee of future performance.