They say nothing in life is certain, except for death and taxes. While neither is avoidable, there may be certain ways to mitigate the impact of taxes at death.

President Joe Biden’s recently proposed “American Family Plan” highlights funding the legislation through increased income and capital gains tax on the wealthiest and highest earning Americans.

What is also being proposed is the elimination of a 100-year-old tax favorable rule known as the step-up in basis, which occurs at death. Currently, if an individual passes away, appreciated assets pass on to heirs with a new tax basis, valued at the time of death. This means if heirs immediately sell inherited assets, they are not subject to capital gains tax.

“What is also being proposed is the elimination of a 100-year-old tax favorable rule known as the step-up in basis, which occurs at death.”

Under the new proposal, gains on appreciated assets would potentially be taxable upon death, even if the heirs plan to hold onto the asset. There would be a $1 million exemption on capital gains, however.

Example: If an individual purchased an asset for $200,000 and the market value of the asset was $2,000,000 upon death, capital gains tax would be due on $800,000 of gain ($2,000,000 market value – $1,000,000 exemption – $200,000 tax basis).

“There are also rumblings of potential changes to the gift and estate tax code.”

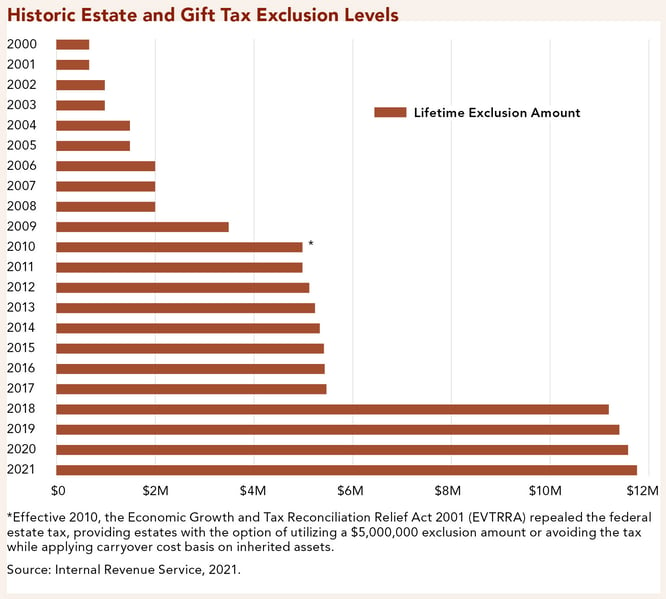

There are also rumblings of potential changes to the gift and estate tax code. Currently, an individual can gift up to $11.7 million over the course of their life—or pass this amount on at death—without paying a dime in gift or estate tax. For married couples, this exemption amount is $23.4 million. Transfers that exceed these amounts are subject to a top estate tax rate of 40%.

Example: If an individual gifts $5 million while living, and he or she passes with an estate valued at $10 million, the total amount excluded is $11.7 million. The additional $3.3 million is subject to estate taxes.

These amounts are slated to revert to a uniform $5.49 million after 2025 (adjusted for inflation) but could be accelerated prior to this date. Biden has indicated that he plans to reduce the federal gift and estate tax exemption amount from a uniform $11.7 million to an estate tax exemption of $3.5 million, including a gift tax exemption of $1 million—with transfers exceeding these amounts subject to a top tax rate of 45%.

Example: If an individual maximizes their lifetime gifting at $1 million, they will have a $2.5 million remaining estate tax exemption at death.

If you combine the elimination of the step-up in basis with lower gift/estate tax exemptions, you may face a very unfavorable tax code. The proposed taxes and long-term impact on multi-generational wealth could be profound.

It may be difficult for Congress to enact both tax changes, but let’s look at a worst-case example of potential tax on a $5,000,000 estate in California with $3,000,0000 in capital gains (see the table below).

Under the current tax laws, this $5,000,000 estate would pass to heirs free of gift, estate, and capital gains taxes.

Another aspect to consider is tax treatment of real estate assets. Currently there is no limit on 1031 exchanges, but a $500,000 limit on nontaxable gains may be imposed in the near future. For primary residences, the existing $250,000 capital gains tax exemption for individuals ($500,000 for married couples) is expected to remain in place.

So, what are some planning areas that you may want to begin discussing with your investment counselor?

LIFETIME GIFTING WHILE EXEMPTION IS $11.7 MILLION

Biden has indicated that he plans to reduce the tax exemption for estates and gifts and increase the rates at which they are taxed to “historic norms.”

If you gift before limits are lowered, the gifting exemption is not expected to be “clawed back” retroactively. Therefore, it may be wise to gift sooner rather than later if the intention is to reduce your gross estate. Keep in mind that when you gift assets, you are relinquishing ownership, control, and use of those assets. It is essential to work with your investment counselor to ensure that all your current and future needs are accounted for before gifting.

“If you gift before limits are lowered, the gifting exemption is not expected to be ‘clawed back’ retroactively.”

There is also an annual gift tax exemption of $15,000 per donor, per recipient. An individual may gift anyone up to $15,000 in assets per year, free of gift taxes.

Example: A couple with three married children and six grandchildren could give away a total of $360,000 per year to these 12 relatives, plus $30,000 to anyone else they choose. Any gifts above the annual exemption are subtracted from the individual’s lifetime gift and estate tax exemption.

Another strategy to consider around gifting may be to make payments directly to medical and education providers on behalf of a loved one as these payments are not considered to be gifts.

<br>

ESTATE PLANNING DOCUMENTS AND STRATEGIES

There are additional asset transfer methods that may effectively reduce the value of your estate. Some of these may include utilizing various legal structures, trust vehicles, charitable planned giving strategies, and real estate options.

Aside from these strategies, it is important to review existing trust documents on a regular basis to determine if updates are needed as a result of any changes within your personal objectives or the tax law.

<br>

IRREVOCABLE LIFE INSURANCE TRUST (ILIT)

A common misconception around life insurance is that the death benefit is not subject to tax. Although proceeds are received by beneficiaries free of income tax, they are included as part of your gross estate, and taxable if the estate value exceeds the exemption amount.

An ILIT creates a tax efficient pathway for wealth transfer using life insurance in conjunction with an irrevocable trust. This strategy removes the insurance policy from the grantor’s gross estate, while still providing liquidity to offset wealth transfer taxes.

Life insurance needs evolve over time and insurance policies should be reviewed and factored into your financial plan like any other asset in your estate.

<br>

DECEASED SPOUSAL UNUSED ELECTION (DSUE)

When a spouse passes away, it may be implied that the surviving spouse automatically receives the deceased spouse’s estate tax exemption (currently $11.7 million). However, this is not the case. To ensure that the unused exemption transfers to the surviving spouse, the executor of the estate should consider electing what is known as the Deceased Spousal Unused Election (DSUE) on an estate tax return (Form 706).

Form 706 is only required if estate assets are above the exemption amount. Therefore, many surviving spouses miss out on this opportunity without proper planning*. This portability election is especially important now that the exemption amounts are at an all-time high, and could decrease significantly with the 2025 sunset provision, or sooner.

Effective wealth planning requires sophisticated strategies implemented in a proactive manner. With potential new legislation on the horizon, now is a great time to review your financial plan with your investment counselor. While we are not attorneys, insurance agents, or tax advisers, Clifford Swan is here to help you navigate the various stages of your life and assemble the appropriate team of professionals to meet your goals, values, and objectives.

* This form is due nine months from the date of death with a six-month automatic extension available.

The above information is for educational purposes and should not be considered a recommendation or investment advice. Investing in securities can result in loss of capital. Past performance is no guarantee of future performance.